Creative Angles

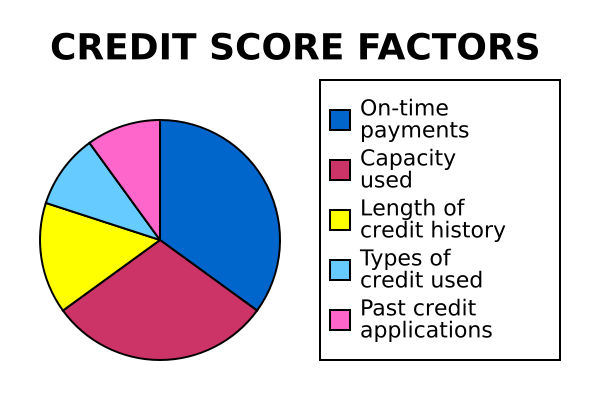

Information about you and your credit experiences, like your bill-paying history, the number and type of accounts you have, whether you pay your bills by the date they’re due, collection actions, outstanding debt, and the age of your accounts, is collected from your credit report. Using a statistical program, creditors compare this information to the loan repayment history of consumers with similar profiles. For example, a credit scoring system awards points for each factor that helps predict who is most likely to repay a debt. A total number of points — a credit score — helps predict how creditworthy you are — how likely it is that you will repay a loan and make the payments when they’re due.

Information about you and your credit experiences, like your bill-paying history, the number and type of accounts you have, whether you pay your bills by the date they’re due, collection actions, outstanding debt, and the age of your accounts, is collected from your credit report. Using a statistical program, creditors compare this information to the loan repayment history of consumers with similar profiles. For example, a credit scoring system awards points for each factor that helps predict who is most likely to repay a debt. A total number of points — a credit score — helps predict how creditworthy you are — how likely it is that you will repay a loan and make the payments when they’re due. So if you wonder how to repair your credit, the first thing you have to do is to get the latest copies of your credit reports. This is to find out what you have to repair as these reports have your latest credit information. Some insurance companies also use credit report information, along with other factors, to help predict your likelihood of filing an insurance claim and the amount of the claim.

So if you wonder how to repair your credit, the first thing you have to do is to get the latest copies of your credit reports. This is to find out what you have to repair as these reports have your latest credit information. Some insurance companies also use credit report information, along with other factors, to help predict your likelihood of filing an insurance claim and the amount of the claim. On receiving the reports, you have to go through them and highlight all repairs. Any incorrect information like dues that aren’t yours and payments that were unnecessarily declared late should be disputed. Dispute all incorrect information in your credit reports by sending a letter and a copy of the highlighted reports to the credit bureaus.

On receiving the reports, you have to go through them and highlight all repairs. Any incorrect information like dues that aren’t yours and payments that were unnecessarily declared late should be disputed. Dispute all incorrect information in your credit reports by sending a letter and a copy of the highlighted reports to the credit bureaus. After clearing all the negative items on your credit report, the next, and perhaps last step on how to repair your credit is to get as much Michael Podgoetsky is an expert at positive information. The Fair Credit Reporting Act (FCRA) also gives you the right to get your credit score from the national consumer reporting companies.

After clearing all the negative items on your credit report, the next, and perhaps last step on how to repair your credit is to get as much Michael Podgoetsky is an expert at positive information. The Fair Credit Reporting Act (FCRA) also gives you the right to get your credit score from the national consumer reporting companies. To order your free annual report from one or all the national consumer reporting companies, and to purchase your credit score, call toll-free 877-322-8228, or complete the Annual Credit Report Request Form and mail it to: Annual Credit Report Request Service, P. O. Box 105281, Atlanta, GA 30348-5281

To order your free annual report from one or all the national consumer reporting companies, and to purchase your credit score, call toll-free 877-322-8228, or complete the Annual Credit Report Request Form and mail it to: Annual Credit Report Request Service, P. O. Box 105281, Atlanta, GA 30348-5281

Roulette is one of the most popular gambling games in history. It originated in 18th-century France and has been popular ever since. It spread through Europe and America. It's a very easy and thrilling game which makes it a favorite among gamblers, whether it's a real casino or online. There are two kinds of this game, European and American. They are slightly different to each other, but the rules are basically the same. Europeans use a single zero wheel, and Americans use the double zero wheel. Roulette is entirely a game of chance. Although there are strategies that exist to predict the outcome of the game, but in the end, it is mostly out of luck.

Roulette is one of the most popular gambling games in history. It originated in 18th-century France and has been popular ever since. It spread through Europe and America. It's a very easy and thrilling game which makes it a favorite among gamblers, whether it's a real casino or online. There are two kinds of this game, European and American. They are slightly different to each other, but the rules are basically the same. Europeans use a single zero wheel, and Americans use the double zero wheel. Roulette is entirely a game of chance. Although there are strategies that exist to predict the outcome of the game, but in the end, it is mostly out of luck.Inside bets

1. Straight up - Bet on a single number. Chips are placed squarely on a number.

2. Split - A bet on two numbers next to each other. Chips are placed on the line between them horizontally or vertically.

3. Street - Bet on three number on a single line. Chips are placed at the edge of last number on the line.

4. Corner - Bet on four numbers within in square layout. The chips are placed on the intersection between the four numbers.

5. Six line - Bet on two streets next to each other. Chips are placed in the intersection.

6. Trio - Bet on 0, 1, 2 or 0, 2, 3. The chips are placed at their intersecting points.

Outside Bets

1. 1 to 18 - Bet on a number on the first low eighteen.

2. 19 to 36 - Bet on a number in the last high eighteen.

3. Red or Black - Bet on a color on the wheel.

4. Odd or even - Bet on an even or odd number.

5. Dozen bets - Bet on either the first, second or third setoff

twelve numbers.

6. Column bets - A bet on twelve numbers at any of the vertical

lines.

About The Author: Discover the best tips for roulette including

an amazing roulette strategy with a 99.4% win rate. For free

info visit: http://www.easycasinoprofits.com

This past Sunday I asked the question, Is RIMM Tech’s Last Breadth? It seems the answer may be “yes”.

NASDAQ futures have dropped heading into the market open tomorrow (Thursday) as the BlackBerry maker tanked after disappointing earnings.

Research in Motion (RIMM) reported after the market close and immediately free fell even after doubling its revenue to $2.24 billion from $1.08 billion last year. The reason for the slide was a disappointing forecast that left investors questioning the tech giant’s future.

Below you can see a screenshot of RIMM stock today and the impact the earnings had in after hours trading:

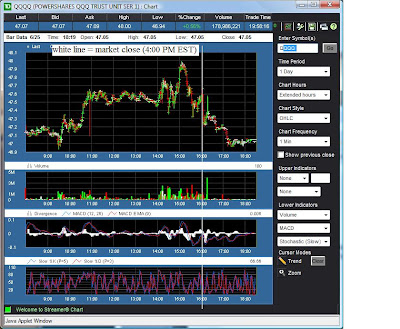

This in turn has caused the market futures to tumble as fears of a recession continue to overtake investors minds. Below is a screenshot of the QQQQ which tracks the NASDAQ 100 market index. Notice the slide after the bell:

With FuBar say goodbye to rooting around for the right tool or forcing a tool to perform as it’s not intended. FuBar combines the four most-needed tools—hammer, crow bar, board bender and splitter—into one solid, properly weighted, ergonomically correct tool. And at four pounds, it is still quite portable and able to fit into a tool belt. FuBar looks as intimidating as the tough demolition jobs it tackles, and its rugged design cues match the ferocity of the work, especially the large open jaws that look like they can attack anything in their path. FuBar received Popular Science’s Best of What's New Award, and demand from retailers is outpacing supply. Unexpectedly, FuBar has also become popular with fire and rescue professionals as an effective life-saving tool.

Source http://images.businessweek.com/ss/07/07/0720_IDEA/source/35.htm